Mid Week Reads: June 7, 2023

Mortgage Rates, Student Loans, and The Debt Ceiling

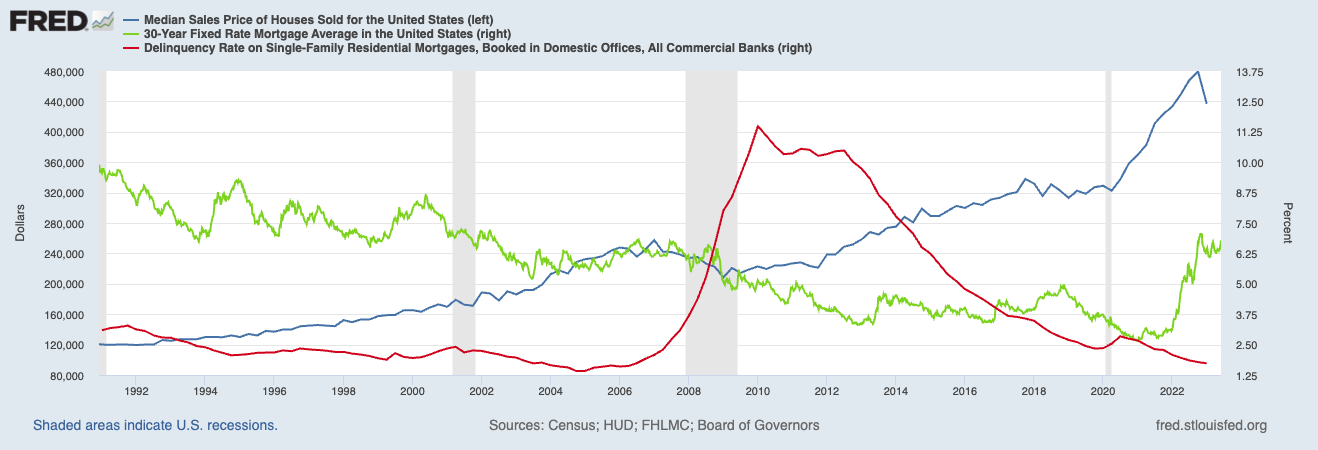

Mortgage Rates & Housing: It’s no secret that interest rates have risen recently. But how much?

Answer: A lot, but not a lot compared to history.

In recent times, it seems like rates have gone very up, very quickly. But compared to 1990, we are actually below those rates. Mortgages are priced based off of the “risk-free” rate set by the yield on government bonds. Our recent sharp increase in interest rates is mainly due to the one of the sharpest rise in central bank interest rate hikes in history.

Mortgage Rates from today to 10 years ago.

Mortgage rates from today to 1990.

Rewind to just after the 2008-2009 housing crash, home prices quickly recovered in large part to quickly declining interest rates and loose monetary policy. Of course, the days of “stated income” and NINJA (no income, no job, no asset) loans were over, but those with provable income and decent credit scores could get a mortgage. With falling and low interest rates for a very long time, a lot of homeowners refinanced or bought a new home and could get a break on the monthly note.

Let’s face it, the houses were not actually worth more in many cases, but the financing was so cheap that it wasn’t worth losing a bidding war over a house you really wanted. So what did people do, they upped the offering price and sale prices went to the moon. I distinctly remember house hunting with my now wife in 2014, most houses we looked at we under contract in 5-10 days and we were constantly fighting with all cash or quick close offers from other buyers willing to waive contingencies or inspections. Fast forward to the present, people are not only not waiving inspections and contingencies, they are adding new ones such as employment contingency, where they can call off the deal if they become unemployed. Unlike 2014, when rates were lower and it was a bidding war, the buyers have the advantage. But that doesn’t mean home prices are dropping like a rock (see chart below, blue line).

**Note: Sometimes people have a “cash” offer if they obtain the cash by taking a second mortgage or HELOC on their current home. This makes the offer more attractive as the buyer can no longer make obtaining financing a contingency of the sale. Another way to do this is through a margin or securities backed line of credit.

what about people who bought homes in the pandemic or refinanced when rates were low?

Well, they feel (are) stuck! It’s no secret. In short, there is now a glut of people who are caught at the four way intersection housing hell: 1) They locked in a low rate and don’t want to lose it, 2) They want to move, 3) Current rates are high, 4) Prices have not dramatically come down due to less houses for sale because of #1. This creates an environment where they can’t afford to buy something similar somewhere else. When rates go up, the monthly payment goes up, unless the sale prices comes down.

Now that interest rates are up, why are we not seeing more people behind on their mortgages if both rates are going up and the economy is cooling?

A combination of people being worried and stuffing their savings accounts, the 30 year fixed rate mortgage, and record low interest rates (until recently). America is unique with the prevalence of the 30 year and 15 year fixed rate mortgage. In many parts of the world, mortgage rates reset every few years. People were able to refinance to a lower rate during the pandemic and maybe saw the writing on the wall with possible layoffs and stuffed their savings accounts. As outlined in the previous paragraph, unless someone buys a new property with a new mortgage or refinances they will not subject themselves to the higher rates. It will be interesting to see how this plays out with student loan payments resuming.

Home prices peaked in late 2022 and the average existing home sale price was $436,000 for Q1 2023. During the COVID-19 pandemic home prices shot up from under $340,000 to $480,000.

Student Loans- They’re Back!

In case you were unaware, student loans are coming back. It was part of the debt ceiling deal. People should begin to find room in their budgets now and start bracing for repayments.

>>>Financial Planning Implication: When you calculate how much you need for emergency savings, we typically tell people to have at least six months of non-negotiable expenses saved. If your payment is $600/mo, that means you need to increase your emergency fund by $3,600 if that payment was not already in the calculation already.